Ceribell (CBLL)·Q4 2025 Earnings Summary

Ceribell Beats Q4 as FDA Clearances Unlock $1.5B+ Market Expansion

February 24, 2026 · by Fintool AI Agent

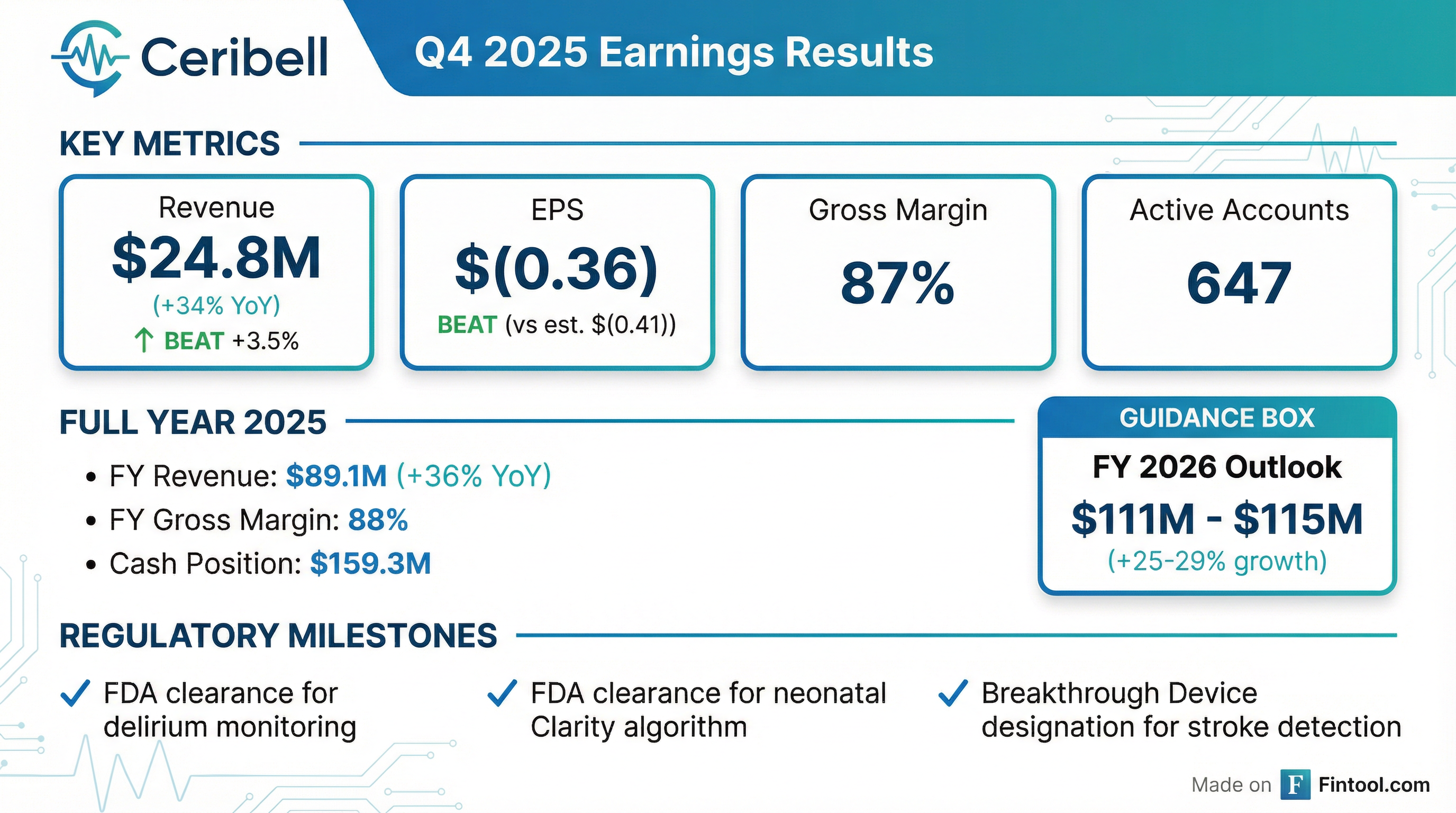

Ceribell delivered another strong beat in Q4 2025, posting $24.8M in revenue (+34% YoY) and narrowing losses to $(0.36) per share, while achieving three transformative FDA clearances that management believes unlock over $1.5B in incremental market opportunity. The point-of-care EEG leader extended its streak to six consecutive revenue beats and raised its account base to 647 active hospitals.

Did Ceribell Beat Earnings?

Yes — beat on both revenue and EPS.

Ceribell has now beaten consensus revenue estimates for six straight quarters since its October 2024 IPO.

The company ended 2025 with $89.1M in total revenue, up 36% from $65.4M in 2024. Product revenue ($67.3M, +34% YoY) and subscription revenue ($21.7M, +41% YoY) both accelerated, reflecting deeper penetration into existing accounts and expansion into new hospitals.

What Did Management Guide?

Ceribell guided FY 2026 revenue of $111M - $115M, representing 25-29% growth over FY 2025.

The guidance midpoint of $113M is essentially in-line with Wall Street's $112.7M estimate. While this represents deceleration from 36% growth in 2025, it comes amid a significantly larger revenue base and follows substantial infrastructure investments made post-IPO.

What Changed From Last Quarter?

Regulatory Breakthrough Quarter

The biggest development was Ceribell's regulatory trifecta:

-

Delirium Monitoring Clearance — First-of-its-kind FDA 510(k) for continuous delirium monitoring. Delirium affects >30% of ICU patients with no current diagnostic device available.

-

Neonatal Clarity Algorithm — FDA 510(k) clearance making Ceribell the first and only seizure detection algorithm cleared for pre-term neonates through adults.

-

Stroke Breakthrough Designation — FDA Breakthrough Device designation for first-in-class large vessel occlusion (LVO) stroke detection and monitoring.

Management believes these clearances unlock incremental market opportunities exceeding $1.5 billion beyond the $2B core seizure detection market.

Account Growth Acceleration

Active accounts grew to 647 at year-end, up 32 accounts sequentially from 615 in Q3 2025. This continues the strong account addition pace seen in 2025, with Q3's 31-account sequential add representing the largest increase since the IPO.

Profitability Path

- Gross margin: 87% in Q4, 88% for FY 2025 — near industry-leading levels

- Cash position: $159.3M, down from $168.5M in Q3 2025

- Management has previously stated commitment to reaching cash flow break-even with cash on hand without additional capital raises

How Did the Stock React?

Earnings were announced after market close on February 24, 2026. The stock closed at $19.90, down 0.4% on the day. The conference call is scheduled for 1:30 PM PT / 4:30 PM ET.

Key price levels:

- 52-week high: $26.04

- 52-week low: $10.01

- 50-day moving average: $21.29

- 200-day moving average: $16.23

The stock has traded in a range of $16-$26 since the IPO, with the current price near the middle of that range.

Key Management Quotes

CEO Jane Chao on the milestone year:

"2025 was a milestone year for Ceribell. We accelerated adoption across new and existing accounts, broadened the age range of our seizure detection algorithm to include pediatric and neonatal populations, and achieved critical regulatory milestones, unlocking incremental market opportunities that we believe exceed $1.5 billion."

On the vision for EEG:

"As we enter the new year, we believe these accomplishments position us well to drive continued growth and advance our long-term vision of making EEG a new vital sign."

Segment Breakdown

Subscription revenue continues to outpace product revenue growth, reflecting increasing utilization within the existing account base. During Q3 2025, management noted utilization per account had increased nearly threefold over the past five years, yet they estimate only 30% penetration within their active accounts.

Market Opportunity & Growth Drivers

Ceribell frames their opportunity across multiple horizons:

Management estimates they are currently at only ~3% penetration of their core U.S. market, with over 5,000 acute care hospitals still without point-of-care EEG.

Forward Catalysts

- Full neonatal Clarity launch — Expected in 2026 with hardware + algorithm commercially available

- VA system expansion — Following successful pilots, VA has indicated plans to expand Ceribell usage across the nearly 200-hospital system

- Delirium commercial strategy — Management indicated they will detail comprehensive commercial vision in coming quarters

- Q4 2025 earnings call — Scheduled for 4:30 PM ET today for additional color on 2026 strategy

Risk Factors

- Competition: Management acknowledged increased competitive activity in 2025, though results have not been materially impacted

- Tariffs: Company has established manufacturing in Vietnam to reduce China tariff exposure; gross margins expected to remain in mid-80s assuming current tariff levels

- ITC litigation: Ongoing intellectual property litigation with expected ruling timeline of September 2026 / January 2027, potentially delayed by government shutdowns

- Profitability: Company remains unprofitable with $53.4M FY 2025 net loss, though path to break-even is articulated

Bottom Line

Ceribell delivered another solid beat in Q4 2025 while achieving transformative regulatory milestones. The triple FDA clearance in delirium, neonates, and stroke dramatically expands the company's addressable market beyond seizure detection. With 88% gross margins, $159M in cash, and only ~3% penetration of their core market, the growth runway remains substantial. The key question for investors is execution timing on these new market opportunities and the path to profitability as the company scales.

Read the full Q4 2025 8-K filing | Company Overview